Ah, retirement . . . that magical time when you’ll wake up whenever you darn well feel like it, send your grandkids to college debt-free, buy that classic Corvette you’ve been drooling over, and go skydiving over New Zealand.

No matter what your retirement dream looks like, it’s going to take money to turn those dreams into a reality. After all, those classic ’Vettes aren’t getting any cheaper (and don’t even get us started on the gas to drive it!). So the more you know about your options for retirement saving, the better.

Your 401(k) and Roth IRA are two of the most powerful tools you can use to save for retirement. You might be a little familiar with both terms, but what are they exactly? And which one will best help you save for retirement? Let’s start with the basics:

- A Roth IRA is an account that allows you to save a certain amount each year for retirement. But what makes a Roth IRA one of the best retirement savings options is that it includes tax-free growth and tax-free withdrawals once you retire.

- A 401(k) is a retirement savings plan that’s sponsored by an employer. With a traditional 401(k), employees decide how much of their paychecks to invest automatically in their account. The money you put in is tax-deferred, meaning you won’t pay income taxes on that money . . . yet. But years from now, when you retire and start pulling from your 401(k) savings, those withdrawals will be taxed at whatever the income tax rate is when you take it out.

The truth is, a Roth IRA and a traditional 401(k) are both great ways to build wealth for retirement, but it’s important to know their differences and how they work together. So let’s break down the pros and cons for both retirement savings options and see which one works best for you. (Hint: It could be both.)

What Is a Roth IRA?

A Roth IRA (Individual Retirement Account) is a retirement savings account you can open yourself. When you hear the word Roth, your ears should automatically perk up—because a Roth IRA allows your savings to grow tax-free. That’s right: tax-free. That means once you turn 59 1/2, you can withdraw money from your account without owing a penny in taxes. Sweet!

Advantages of a Roth IRA

Here are some advantages a Roth IRA has over a traditional 401(k):

Tax-Free Growth

Unlike a traditional 401(k), you contribute to a Roth IRA with after-tax dollars. Translation? Since you invest in your Roth IRA with money that’s already been taxed, the money will grow tax-free inside the account and you won’t pay a dime in taxes when you withdraw your money at retirement.

And here’s the deal: Once you’re ready to retire, most of the money in your Roth IRA will be growth. So, no taxes on that growth means hundreds of thousands of dollars stay in your pocket and out of Uncle Sam’s!

More Investing Options

With a Roth IRA, you’re not limited by some third-party administrator deciding which funds you can invest in—you literally have thousands of mutual funds to pick and choose from. When you have more options, you have more power to make good choices.

Not Tied to Your Employer

Unlike a workplace retirement plan, you can open a Roth IRA at any time. And no matter what your employment situation is, it doesn’t affect your Roth IRA at all. No need to roll over anything or worry about keeping track of a pile of 401(k)s you left behind from old jobs.

No Required Minimum Distributions (RMDs)

With a Roth IRA, you can keep your money in the account forever if you’d like. That means you can let more of your money keep growing over a longer period of time.

The Spousal IRA

If you’re married but only one of you earns money, you can still open a Roth IRA for the nonworking spouse. The spouse who earns money can invest in accounts for both spouses—up to the full amount! On the other hand, only the employee of the company offering a 401(k) can contribute to their 401(k).

Disadvantages of a Roth IRA

The Roth IRA sounds pretty awesome, doesn’t it? But it does have some limitations you need to know about:

Lower Contribution Limits

You can only invest up to $7,000 in a Roth IRA in 2024 (or $8,000 if you’re age 50 or older).1 When you compare that with the 401(k) contribution limit ($23,000 for 2024), you might be thinking, That’s it? Yep. That’s why 401(k)s and Roth IRAs work better together.

Income Limits

As amazing as the Roth IRA is, there’s a chance you might not even be eligible to put money into one. Gasp! If your modified adjusted gross income (MAGI) is higher than $161,000 as a single person or more than $240,000 as a married couple filing jointly, you won’t be able to contribute to a Roth IRA in 2023.2 But don’t worry, the traditional IRA is still an option—it’s better than nothing.

The Five-Year Rule

This won’t be an issue for most folks, but the five-year rule says you can’t take money out of your Roth IRA until it’s been at least five years since you first contributed to the account. You’ll get hit with taxes and penalties if you break that rule (so don’t do that).

Market chaos, inflation, your future—work with a pro to navigate this stuff.

And remember: Just like the 401(k), you’ll be penalized for taking money out of a Roth IRA before age 59 1/2 (don’t do that, either).

Now that we’ve broken down the Roth IRA, let’s turn our attention to the pros and cons of the 401(k). Then we’ll compare the two and see if there’s a winner.

What Is a 401(k)?

A 401(k) is a retirement savings plan many employers offer as a way to encourage employees to save for retirement. Basically, you tell your employer how much you want to invest in your 401(k)—usually as a percentage of your salary or a specific amount each pay period—and that money is automatically taken out of your paycheck and put into retirement savings. Voila!

According to The National Study of Millionaires, 8 out of 10 millionaires built their wealth through their company’s 401(k). If all those people used a boring old 401(k) to get to millionaire status, you can too!

Advantages of a 401(k)

Let’s take a look at some of the main advantages of a 401(k):

Higher Contribution Limits

In 2024, you can invest up to $23,000 in a 401(k), 403(b) or in most 457(b) plans—including the employer match (keep reading for more on that). That’s a lot of money! If you’re 50 or older, you can add an additional $7,500 per year, for a total of $30,500.3

Employer Match

This is the big one. Probably the best thing about a 401(k) plan is that your employer can match your investment up to a certain amount. That’s a 100% return on your investment right off the bat. Matching isn’t required by the government, so not all employers offer it. If yours does, make the most of it. Don’t overlook free money!

Lower Taxable Income

Since you invest in your traditional 401(k) with pretax dollars, that means you’ll pay less in income taxes when tax season rolls around. Sorry, not sorry, Uncle Sam!

You Can Take It With You

And here’s some peace of mind: The money you invest in your 401(k) is all yours. You can roll over your 401(k) account to an IRA if you get a new job or your company goes out of business.

Disadvantages of a 401(k)

Your 401(k) is a great way to save for retirement, but you also need to understand a few of its shortcomings too:

Fewer Options for Mutual Funds

Employers usually hire a third-party administrator to run their company’s retirement plan. That administrator picks and chooses which mutual funds to offer in the plan, which limits your options. Womp womp.

Withdrawals in Retirement Will Be Taxed

Remember those tax breaks you get on your traditional 401(k) contributions? (Yeah, we’ve talked about this already—but that’s because it’s really important.) Well, there’s a catch.

Since you fund a 401(k) with pretax dollars, you won’t pay taxes now—but you will pay taxes on that money in retirement. This could lead to a pretty hefty tax bill depending on what tax bracket you’re in when you retire.

Required Minimum Distributions (RMDs)

You can’t leave your money in your 401(k) forever. Beginning at age 72 (or 73 if you turn 72 in 2023 or later), you must start withdrawing a certain amount of your savings each year or you’ll pay a penalty.4 There are also penalties for withdrawing money before age 59 1/2. Either way, Uncle Sam wants his share!

Waiting Period

If you’re new to a company, you may have to wait a certain length of time to participate in a 401(k) plan or receive an employer match. That’s not great, but some things are worth the wait.

Make an Investment Plan With a Pro

SmartVestor shows you up to five investing professionals in your area for free. No commitments, no hidden fees.

Ramsey Solutions is a paid, non-client promoter of participating pros.

Roth IRA vs. 401(k): What Are the Major Differences?

Okay, folks, does anybody else feel like they’ve been drinking water from a firehose? That was a lot of information! Let’s break it down. Here’s how a Roth IRA and a 401(k) stack up against each other:

|

Feature |

Traditional 401(k) |

Roth IRA |

|

Eligibility |

It’s only available through employer-sponsored programs. There might be a waiting period before you can enroll. |

You must have earned income, but restrictions apply above a certain income based on your filing status. Married couples with only one income earner can also open a spousal Roth IRA. |

|

Taxes |

Contributions are made with pretax dollars, lowering your taxable income. You’ll pay taxes on any money you withdraw in retirement. |

Contributions are made with after-tax dollars, allowing investments to grow tax-free. You won’t pay taxes on withdrawals in retirement. |

|

Contribution Limits |

The 2024 limit is $23,000 per year ($30,500 per year for those 50 or older). Additional contribution limits may apply to highly compensated employees. |

The 2024 limit is $7,000 per year ($8,000 per year for those age 50 or older). |

|

Employer Contribution |

Many employers offer a match based on a percentage of your gross income. |

There’s no matching contribution. |

|

Required Minimum Distributions (RMDs) |

Beginning at age 72 (or 73 if you turn 72 after Dec. 31, 2022), you have to start taking out a certain amount each year to avoid penalties. |

No RMDs—the money can sit in your account as long as you live and you can also leave it as an inheritance. |

|

Investment Menu |

The account is controlled by a third-party administrator who handles (and limits) investment options. |

You have a wider variety of investment options and more control over how you invest. |

|

Penalties |

There are penalties for withdrawals before age 59 1/2. |

There are penalties for withdrawals before age 59 1/2. |

How to Make a 401(k) and Roth IRA Work Together

Okay, so here’s the moment of truth: Should you put your money in a 401(k) or a Roth IRA? The answer is . . . yes!

If you’re eligible for a 401(k) and a Roth IRA, the best-case scenario is that you invest in both accounts (and if you can max them both out—knock yourself out). That way, you’re taking advantage of your employer match and getting the tax benefits of a Roth IRA.

The best way to remember where to start is with this rule: Match beats Roth beats traditional. An employer match is free money, and you simply don’t leave free money on the table—so that’s where you start.

After that, use a Roth IRA instead of a traditional IRA to get those tax benefits. You won’t have to pay taxes when you withdraw money from a Roth IRA, and that’ll pay off more in the long run!

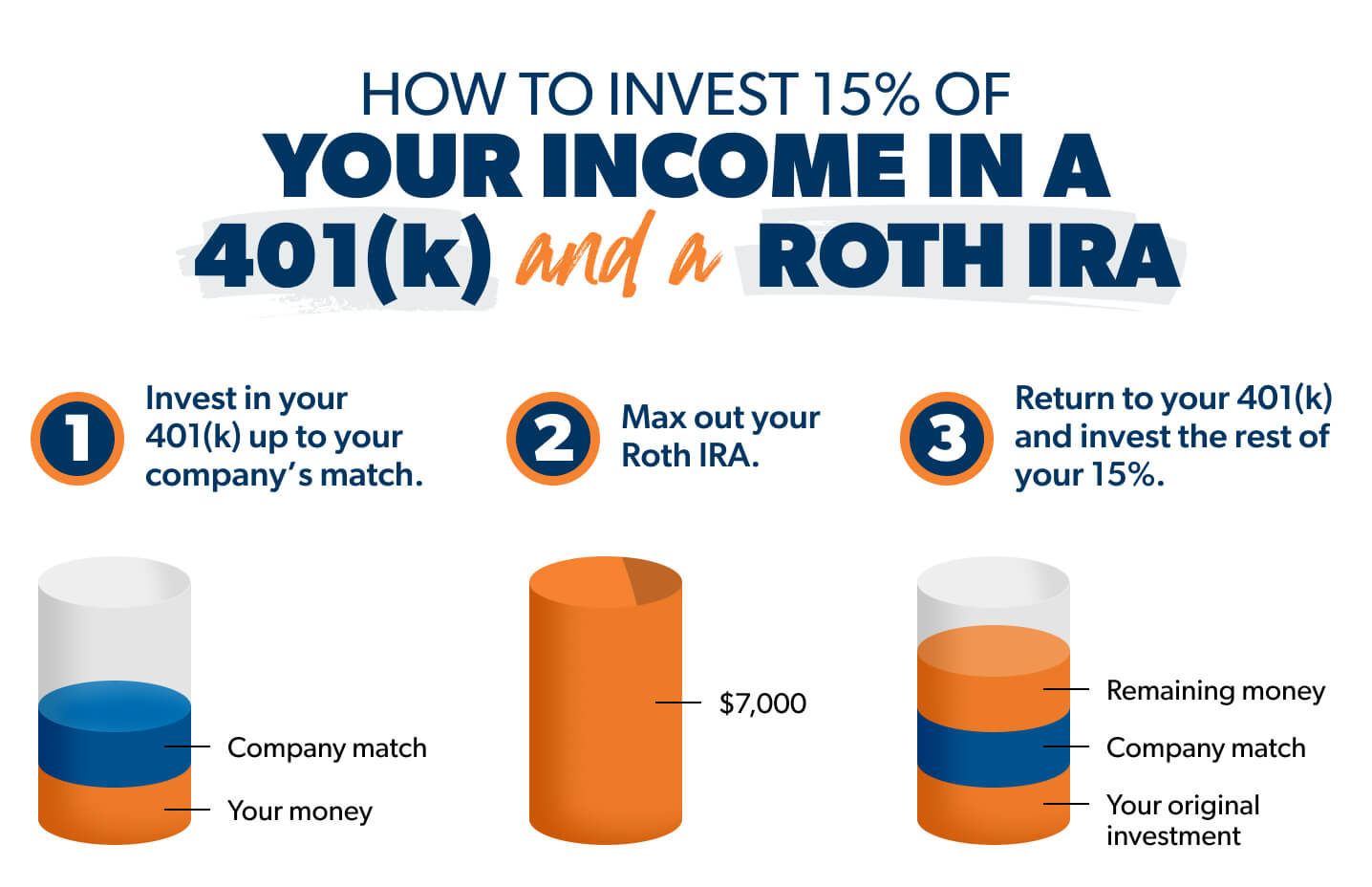

Here’s how that works in three simple steps: Let’s say you make $60,000 a year and you’re under 50. Once you’re debt-free and have a fully funded emergency fund, your goal is to invest 15%—$9,000 in this case—for retirement.

- Start by investing in your 401(k) up to the match your company offers. Let’s say your company offers a 3% match ($1,800). You invest $1,800 in your 401(k) to reach the employer match. This leaves you with $7,200 more to invest.

- Then max out your Roth IRA. You can only contribute $7,000 in 2024, so that leaves you with $200.

- Return to your 401(k) and invest the remaining $200.

If you’re older than 50 and behind on your retirement savings, you can make catch-up contributions to max out your Roth IRA at $8,000 and your 401(k) at $30,500 in 2024.

Oh, and remember this about the employer match on your 401(k): While it’s nice to have, don’t count it toward your 15% goal. Think of it like icing on the cake of your own contributions.

Here’s one more thing to keep in mind: More companies are starting to offer a Roth 401(k) option, which combines many of the benefits of a 401(k) and a Roth IRA. If you work at a company with a Roth 401(k), that makes your situation a lot easier. If you like your investment choices in the plan, you can simply invest your entire 15% in your Roth 401(k) and you’re done!

The Best Choice

So, to sum it all up: Your best choice is to invest in your 401(k) up to the employer match and then open up a Roth IRA—and make sure you reach your goal to invest 15% of your gross income in retirement.

Always seek good advice and invest in good growth stock mutual funds with a history of strong returns. They’re the best way to use the power of the stock market to build wealth over the long term. And steer clear of trendy, “sophisticated” stuff like the latest hot single stock, precious metals or cryptocurrency. Keep things simple and never invest in anything you don’t understand!

Here’s the deal: Investing is worth the hard work. If you don’t save and invest now, you won’t have anything to live on in retirement. It’s a big goal, but you don’t have to do this alone.

Next Steps

- Are you taking advantage of your company’s 401(k) match? If not, get in touch with your company’s 401(k) administrator or HR department and get started. We generally recommend doing that once you’re out of debt and have a fully funded emergency fund.

- Use our investment calculator to help you calculate how much money you can save up for retirement based on how much you’re investing every month.

- If you want help opening up a Roth IRA or picking investments, get in touch with an investment pro through the SmartVestor program.

Frequently Asked Questions

-

At what age does a Roth IRA make sense?

-

There’s no magical number here, folks. You can open and start contributing to a Roth IRA no matter how old or young you are. Yep, there’s no age restrictions as long as you’re earning an income (and as long as your income is below a certain amount).5 It’s never too early or too late to start investing for your retirement!

But if you’re still in debt or don’t have an emergency fund, press pause on saving for retirement until you’re out of debt with a fully funded emergency fund of 3–6 months of expenses. Then you can start investing 15% of your income for retirement with your employer’s 401(k) plan and a Roth IRA.

-

What are the tax advantages of a Roth IRA?

-

This is really where the Roth IRA shines! When you make after-tax contributions to a Roth IRA, it means you’ve already paid taxes on the money you save for retirement, which helps your savings grow faster because they grow tax-free.

Then, when you retire and start withdrawing from your Roth IRA, guess what? You won’t owe Uncle Sam a penny, no matter how much it’s grown. That’s the beauty of a Roth IRA. Think of it as a warm sweater that holds your investments over the years and shields them from taxes.

-

What are the tax advantages of a 401(k)?

-

Unlike a Roth IRA, a traditional 401(k) offers tax benefits on the front end. Your contributions go in tax-deferred, which lowers your taxable income and gives you a tax break for the year. But you’ll pay taxes on any withdrawals you take out at retirement . . . that includes all your contributions, your employer’s contributions, and all the growth your investments earned over the years too. Bummer.

But if your employer offers a Roth 401(k) plan, it has completely different tax benefits. We’ll explore those below.

-

How is a Roth 401(k) different from a traditional 401(k)?

-

We’ve already discussed how a 401(k) is different from a Roth IRA, but some employers might offer you a Roth 401(k), which is great news! We’re big fans of a Roth 401(k).

Like the traditional 401(k), it’s another type of retirement savings plan offered by employers. But there’s one important difference—Roth 401(k) contributions are made after taxes have been taken out of your paycheck. So the money you put into your Roth 401(k) grows (drumroll, please . . .) tax-free! And when you retire, your withdrawals will also be tax-free. Now, that’s a great deal.

So the money you put into your Roth 401(k) grows (drumroll, please . . .) tax-free! And when you retire, that portion of your withdrawals will also be tax-free (you’ll still pay taxes on your employer match and that money’s growth). Now, that’s a great deal.

-

What is a backdoor Roth IRA?

-

A backdoor Roth IRA isn’t actually a different kind of Roth IRA account than what we’ve been talking about. It’s just a term describing a Roth IRA investment strategy for people who are high-income earners. See, a Roth IRA has income limits, and that can keep high-income earners from directly contributing to, or even opening, a Roth IRA.

For example, if you’re filing as single, the income limit for contributing the full amount ($7,000 for 2024 and $8,000 if you’re 50 or older) is $146,000. If you’re filing as married filing jointly, the income limit for contributing the full amount is $230,000.1

So, what do you do if you’re over the income limit? You can go through the back door by first putting your money into a traditional IRA (because it has no income limit) and then converting the account over to a Roth IRA. It might sound sneaky, but it’s perfectly legal! And because you’re transferring money from a traditional to a Roth IRA, you pay the taxes on that money now so your money can grow tax-free in the Roth. No taxes on the withdrawals when you retire? Nice!

This article provides general guidelines about investing topics. Your situation may be unique. If you have questions, connect with a SmartVestor Pro. Ramsey Solutions is a paid, non-client promoter of participating Pros.

Did you find this article helpful? Share it!

About the author

Ramsey